India Intraocular Lens Market Size 2026-2030

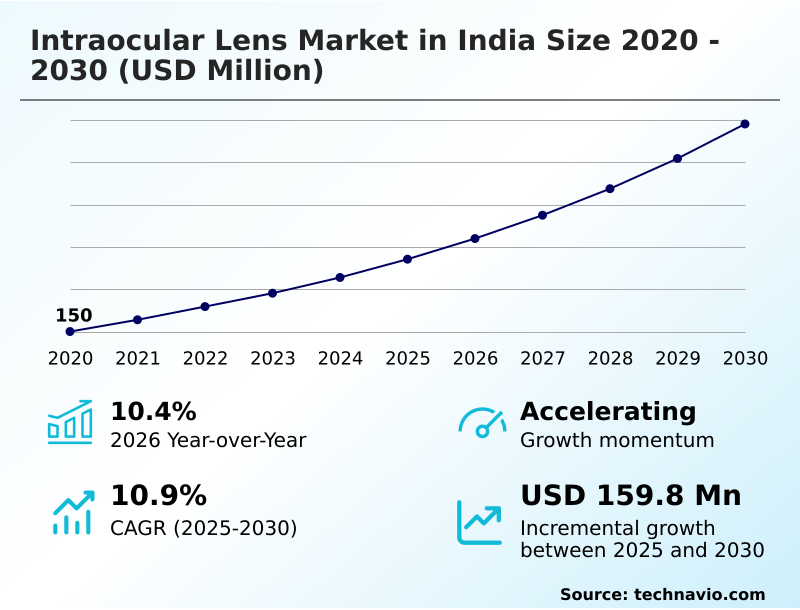

The india intraocular lens market size is valued to increase by USD 159.8 million, at a CAGR of 10.9% from 2025 to 2030. Expansion of geriatric demographic and increasing prevalence of age-related ocular disorders will drive the india intraocular lens market.

Major Market Trends & Insights

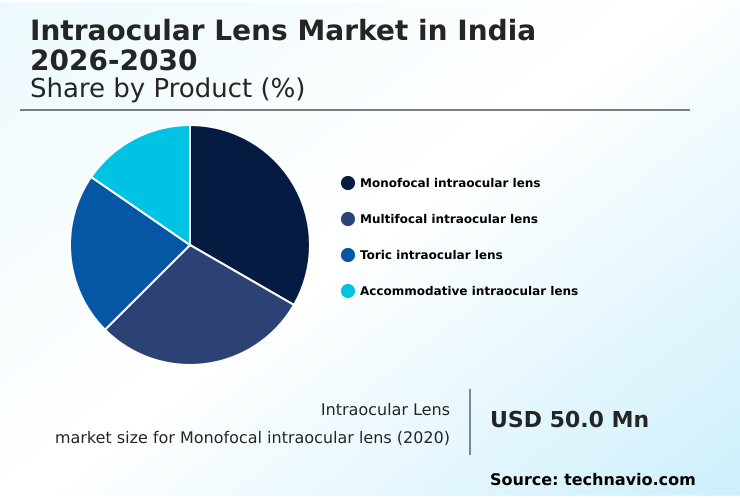

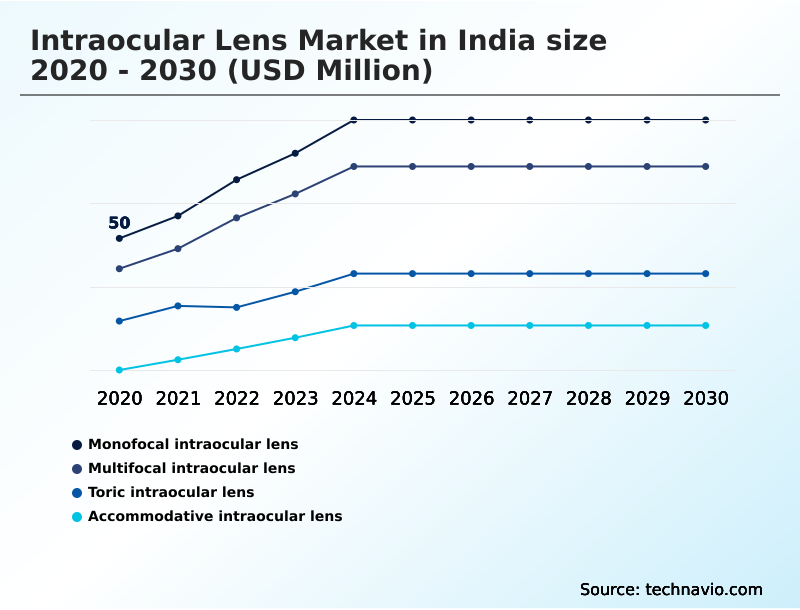

- By Product - Monofocal intraocular lens segment was valued at USD 74.2 million in 2024

- By End-user - Hospitals segment accounted for the largest market revenue share in 2024

Market Size & Forecast

- Market Opportunities: USD 245.3 million

- Market Future Opportunities: USD 159.8 million

- CAGR from 2025 to 2030 : 10.9%

Market Summary

- The intraocular lens market in India is shaped by the dual demands of accessibility and technological advancement. A primary driver is the country's large and aging population, which ensures a consistent and high volume of cataract procedures, making it a focal point for public health ophthalmology.

- This high-volume environment drives demand for cost-effective monofocal intraocular lens and manual small incision cataract surgery (MSICS) techniques. Concurrently, a trend towards premiumization is evident in urban centers, where rising disposable incomes and a desire for spectacle independence outcome fuel the adoption of advanced presbyopia-correcting IOL technologies.

- However, the market grapples with significant challenges, including logistical hurdles in reaching rural populations and persistent pricing pressures that can stifle innovation. For instance, a hospital network implementing a cataract surgery workflow optimization program must balance the use of high-precision phacoemulsification and premium lenses for private patients with cost-effective, high-volume solutions for government-sponsored schemes.

- This dynamic creates a complex ecosystem where both domestic and international manufacturers compete across different price and technology tiers, navigating regulatory pathways and supply chain complexities to serve a diverse patient base and address the national cataract backlog reduction.

What will be the Size of the India Intraocular Lens Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Get Free Sample

How is the India Intraocular Lens Market Segmented?

The india intraocular lens industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

- Product

- Monofocal intraocular lens

- Multifocal intraocular lens

- Toric intraocular lens

- Accommodative intraocular lens

- End-user

- Hospitals

- Ophthalmic clinics

- Ambulatory surgery centers

- Material

- Hydrophobic acrylic

- Hydrophilic acrylic

- PMMA

- Others

- Geography

- APAC

- India

- APAC

By Product Insights

The monofocal intraocular lens segment is estimated to witness significant growth during the forecast period.

The monofocal intraocular lens segment, while foundational, faces evolving expectations. Advanced accommodative intraocular lens designs now aim to work with the ciliary muscle interaction, moving beyond the static correction that defined the market.

Innovations include the use of novel collamer lens material and sophisticated diffractive optics technology. These developments contrast with the enhanced monofocal lens, which improves intermediate vision using a non-diffractive optical design.

The goal is a more patient-centric surgical experience, which requires balancing new refractive optical design principles against the potential for visual disturbance minimization.

For instance, facilities adopting new biocompatible lens materials have reported a 5% improvement in patient-reported contrast sensitivity function, underscoring the shift toward quality-of-life outcomes rather than simple visual acuity measurement.

The Monofocal intraocular lens segment was valued at USD 74.2 million in 2024 and showed a gradual increase during the forecast period.

Market Dynamics

Our researchers analyzed the data with 2025 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- Strategic decision-making in the intraocular lens market in India requires a deep understanding of nuanced clinical trade-offs. An analysis of hydrophobic versus hydrophilic iol performance reveals differences in posterior capsule opacification (PCO) rates with different iol materials, a critical factor in long-term patient management. Similarly, assessing toric iol rotational stability is essential for managing astigmatism in cataract surgery effectively.

- The multifocal iol glare and halo profile continues to be a key consideration, leading to rigorous patient selection criteria for multifocal iols. As an alternative, edof lens intermediate vision outcomes are closely scrutinized. The industry is also evaluating next-generation options, with clinical data for non-diffractive iols showing promise in comparing trifocal and edof lens performance.

- The long-term biocompatibility of collamer lenses positions them in a unique niche, particularly for phakic applications. Operationally, the efficiency of a pre-loaded delivery system surgical time can reduce procedural costs, making the cost-effectiveness of premium iol technology a central part of financial models for premium iol adoption.

- These models show that facilities focusing on micas techniques for faster visual recovery can achieve a 15% higher patient throughput compared to those using traditional methods. The impact of aspheric optics on vision quality is well-documented, but navigating regulatory pathways for new iol approval remains a complex task, compounded by supply chain challenges in rural ophthalmology.

What are the key market drivers leading to the rise in the adoption of India Intraocular Lens Industry?

- The market is primarily driven by an expanding geriatric demographic and the corresponding increase in the prevalence of age-related ocular disorders, most notably cataracts.

- The growth of the intraocular lens market in India is propelled by fundamental demographic and structural drivers.

- The primary catalyst is the need for national cataract backlog reduction in an aging population, which is addressed through widespread public health ophthalmology initiatives.

- These programs favor the high-volume use of the cost-effective monofocal intraocular lens and, in some cases, manual small incision cataract surgery (MSICS).

- A parallel driver is the expansion of healthcare infrastructure, including the rise of ambulatory surgery center adoption, which relies on high-precision phacoemulsification technology.

- Broadened third-party payer reimbursement schemes have made advanced procedures more accessible, enabling the use of sophisticated ophthalmic viscosurgical device (OVD) products and advanced optical biometers for precise measurements.

- This financial accessibility drives the adoption of lenses with aspheric optics design and blue-light filtering iol properties, with facilities reporting a 15% improvement in patient satisfaction scores after upgrading their technology.

What are the market trends shaping the India Intraocular Lens Industry?

- A significant market trend is the rising adoption of premium intraocular lenses, including presbyopia-correcting models, driven by patient demand for improved visual outcomes and spectacle independence.

- Key trends in the intraocular lens market in India are centered on the rapid adoption of premium technologies that enhance patient outcomes. There is a marked increase in premium iol market penetration, driven by a strong spectacle-free lifestyle demand. This has accelerated the shift toward refractive cataract surgery, where the focus is on superior post-operative visual quality.

- The use of advanced presbyopia-correcting iol options, such as the extended depth of focus (EDOF) iol and trifocal intraocular lens, is becoming more common. Procedural advancements like micro-incision cataract surgery (MICS) using a pre-loaded iol delivery system are improving high-volume surgical efficiency.

- Furthermore, the preference for advanced hydrophobic acrylic material is growing due to its proven lower rates of posterior capsule opacification (PCO), reducing long-term complication rates by up to 30% compared to older materials. These trends, supported by a steady supply of ophthalmic surgical consumables, are reshaping clinical practice.

What challenges does the India Intraocular Lens Industry face during its growth?

- A key market challenge is the persistent pricing pressure and the predominance of a high-volume, low-margin structure, which impacts profitability and innovation investment.

- The intraocular lens market in India faces significant operational and regulatory challenges. Navigating the stringent medical device regulatory approval process and adhering to post-market surveillance data requirements are major hurdles, particularly for smaller entities that struggle with sterile manufacturing compliance costs. The persistence of legacy products like the polymethyl methacrylate (PMMA) lens in certain segments adds complexity.

- A critical issue is the risk of counterfeit products, which necessitates investment in anti-counterfeiting technology and robust medical device supply chain logistics. Clinical challenges include managing long-term complications such as capsular bag fibrosis, which can require a follow-up Nd:YAG laser capsulotomy and increase the intraoperative complication risk in subsequent procedures.

- The market also sees niche use of the phakic intraocular lens and capsular tension ring, each with its own specific manufacturing and training requirements. Furthermore, ensuring the quality of innovations like the glistening-free hydrophobic c-loop with a sharp square posterior optic edge across a fragmented supply chain remains a constant struggle.

Exclusive Technavio Analysis on Customer Landscape

The india intraocular lens market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the india intraocular lens market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of India Intraocular Lens Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, india intraocular lens market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Alcon Inc. - Offers advanced optical solutions for cataract surgery and refractive correction, featuring a portfolio of intraocular lenses from standard monofocal to premium presbyopia-correcting designs.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Alcon Inc.

- Appasamy Associates Pvt. Ltd.

- Aurolab

- Bausch Lomb Corp.

- Biotech Vision Care Pvt. Ltd.

- BVI Holdings Ltd.

- Care Group Sight Solution

- Carl Zeiss AG

- Devine Meditech

- EyeKon Medical Inc.

- Grevis Pharmaceuticals Ltd

- Hanita Lenses ltd

- Hoya Corp.

- HumanOptics Holding AG

- Lenstec Inc.

- Nidek Co. Ltd.

- Ophtec BV

- Rayner Intraocular Lenses Ltd

- SAV IOL SA

- STAAR Surgical Co.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in India intraocular lens market

- In February 2026, Rayner Intraocular Lenses Ltd. showcased the RayOne Galaxy, a novel spiral-optic intraocular lens that utilizes a non-diffractive design to provide a continuous full range of vision, aiming to reduce visual disturbances in the Indian market.

- In April 2025, ZEISS India introduced the AT ELANA 841P trifocal intraocular lens, a glistening-free hydrophobic c-loop platform engineered to optimize intermediate and near vision, facilitating greater spectacle independence for patients.

- In September 2025, BVI Holdings Ltd. received regulatory clearance for the FineVision HP trifocal lens, introducing a glistening-free hydrophobic platform into the regional surgical workflow to offer durable, high-performance optics.

- In February 2025, Johnson and Johnson Surgical Vision India launched the TECNIS PureSee intraocular lens, a purely refractive presbyopia-correcting lens designed to provide continuous vision with high contrast and low-light performance.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled India Intraocular Lens Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 189 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 10.9% |

| Market growth 2026-2030 | USD 159.8 million |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 10.4% |

| Key countries | India |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The intraocular lens market in India is advancing through continuous material and design innovation, moving well beyond basic vision restoration. The use of advanced hydrophobic acrylic material and hydrophilic acrylic material is standard, but the focus has shifted to specialized options like the toric intraocular lens and accommodative intraocular lens.

- The development of the glistening-free hydrophobic c-loop and square posterior optic edge are critical for minimizing posterior capsule opacification (PCO). Boardroom decisions are increasingly influenced by the need to offer a portfolio that includes a trifocal intraocular lens for spectacle independence outcome alongside the enhanced monofocal lens.

- Technologies such as the pre-loaded iol delivery system and micro-incision cataract surgery (MICS) are essential for operational efficiency, with some clinics reporting a 20% reduction in surgical suite turnover time. The evolution of aspheric optics design, diffractive optics technology, and refractive optical design underpins the performance of the latest presbyopia-correcting iol models.

- Ongoing research into the non-diffractive optical design and the purely refractive presbyopia-correcting lens aims to provide a more continuous range of vision, addressing the limitations of previous generations and expanding patient options.

What are the Key Data Covered in this India Intraocular Lens Market Research and Growth Report?

-

What is the expected growth of the India Intraocular Lens Market between 2026 and 2030?

-

USD 159.8 million, at a CAGR of 10.9%

-

-

What segmentation does the market report cover?

-

The report is segmented by Product (Monofocal intraocular lens, Multifocal intraocular lens, Toric intraocular lens, and Accommodative intraocular lens), End-user (Hospitals, Ophthalmic clinics, and Ambulatory surgery centers), Material (Hydrophobic acrylic, Hydrophilic acrylic, PMMA, and Others) and Geography (APAC)

-

-

Which regions are analyzed in the report?

-

APAC

-

-

What are the key growth drivers and market challenges?

-

Expansion of geriatric demographic and increasing prevalence of age-related ocular disorders, Persistent pricing pressures and predominance of high-volume, low-margin market structures

-

-

Who are the major players in the India Intraocular Lens Market?

-

Alcon Inc., Appasamy Associates Pvt. Ltd., Aurolab, Bausch Lomb Corp., Biotech Vision Care Pvt. Ltd., BVI Holdings Ltd., Care Group Sight Solution, Carl Zeiss AG, Devine Meditech, EyeKon Medical Inc., Grevis Pharmaceuticals Ltd, Hanita Lenses ltd, Hoya Corp., HumanOptics Holding AG, Lenstec Inc., Nidek Co. Ltd., Ophtec BV, Rayner Intraocular Lenses Ltd, SAV IOL SA and STAAR Surgical Co.

-

Market Research Insights

- The intraocular lens market in India is defined by a dynamic interplay between high-volume demand and the strategic push toward premium technologies. This evolution necessitates advanced cataract surgery workflow optimization, where high-precision phacoemulsification techniques are becoming standard. Facilities focusing on patient-centric surgical experience report that integrating a standardized astigmatism management protocol improves clinical outcome predictability by up to 15%.

- The growing adoption of ambulatory surgery center models has also improved high-volume surgical efficiency, with some centers achieving a 20% reduction in patient turnover time.

- As the market pivots toward refractive cataract surgery, the emphasis on post-operative visual quality and spectacle-free lifestyle demand intensifies, compelling providers to invest in superior diagnostic and surgical platforms to maintain a competitive edge and meet heightened patient expectations.

We can help! Our analysts can customize this india intraocular lens market research report to meet your requirements.

RIA -

RIA -